Cross-collateralising securities is a tongue twister that you need to wrap your head around, as the structure of your home loans can cause headaches if not done correctly. We’re going to break down what cross-collateralising means, what are the pros and cons, and what is the alternative to cross-collateralising.

Cross-collateralising is also known as cross-securitising, which is only a fraction easier to say. Firstly we’ll break down the terms so we have the basics. Collateral is the same as security. It means the goods that are being held as an IOU if you fail to meet your repayments to the lender. Your home loan is secured to your house, if you don’t pay your loan the lender will sell your home and use the proceeds to pay off your debt.

When we talk about cross-collateralising, we’re considering more than one security. When we cross them, we combine their total and effectively pool the security together. You then have a single loan for each purpose under that pooled value.

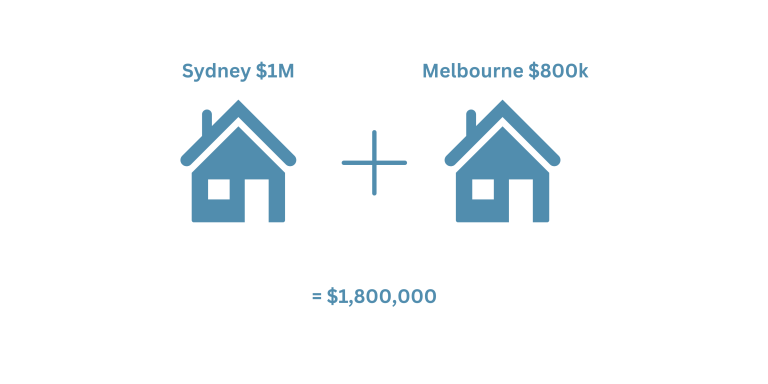

Here’s an example:

I own an investment property in Sydney for $1,000,000 and my home in Melbourne for $800,000. The combined security is worth $1,800,000.

I have a loan of $440,000 on Melbourne, and $1,000,000 for Sydney.

Underneath the umbrella of security at $1.8M, there are two loans:

- $1,000,000 (Sydney)

- $440,000 (Melbourne)

The total loan-to-value ratio (LVR) is $1.44M/$1.8M = 80%

Pros:

- These two accounts allow my Accountant to track my tax-deductible interest expenses for each of my properties.

- It’s a simple and convenient structure, I can see two accounts on my internet banking and know which one is for what.

- Having both loans at the same bank I am offered a better discount because the combined lending is a high amount.

- I was able to borrow 100% of the value for Sydney, by using equity in Melbourne.

- Application was simple with only one application required

Cons:

- The LVR is maxed out at 80% (without LMI) so I can’t use any more equity to buy any more properties until I pay down the principal or values increase

- I don’t have flexibility to refinance one loan away to get a better rate somewhere else, they’re tied together

- If I want to sell Melbourne, I need to ask the bank’s permission and I need to reduce the debt on Sydney to 80% of the value of the remaining security

Let’s break down that last con, as it’s the most common problem;

I want to sell my Melbourne property, but that would mean there is $1,000,000 of Sydney debt remaining on a $1,000,000 security. The bank will not allow a 100% LVR, so we order a valuation on Sydney to determine the current value. If it remains at $1M, I must use the proceeds of my Melbourne sale to reduce the loan to 80% LVR = $800,000. If the value has increased to $1.25M, I can leave the Sydney loan to “standalone” at $1,000,000.

The worst case scenario is that instead of increasing in value, your property declines in value. That could affect how much of your net proceeds you get to keep.

If, by selling one of the crossed properties, your LVR was to increase the bank may require a full application and assessment of your financial position in order to release the security. If your financial position has changed, like you’re in a period of reduced income due to career change, study, or growing a family, you could find yourself stuck and at the mercy of the bank.

Now let’s see the alternative to the cross-collateralising strategy.

Security: Melbourne $800,000

LVR 80%

Loan 1. $440,000 (Purpose: Melbourne)

Loan 2. $200,000 (Purpose: Sydney)

Security: Sydney $1,000,000

LVR 80%

Loan 1. $800,000 (Purpose: Sydney)

If you were to sell Melbourne, we have a similar scenario to the cross collateralisation where you need to pay the extra $200,000 to cover the Sydney loan. But if we take the worst case scenario where Sydney has decreased in value, our calculations aren’t affected because Sydney is standalone and can remain that way.

Pros:

- Risk is mitigated if property declines in value

- Flexibility to sell either property at any time

- Can choose two different banks if I want to

Cons:

- May not be getting full rate discounts if the total lending not with one bank

- Two applications required, more time and paperwork invested

One last example to demonstrate how many homeowners use their equity to start their investment portfolio.

I built my home 10 years ago and have a debt remaining of $300,000. I was lucky enough to build before the big COVID boom, and my house value has now increased to $1,000,000.

My LVR is 30%, and I can access equity up to 80% which gives me a total of $500,000 of equity I can unlock.

I buy a regional investment property worth $400,000 and use my equity in my home to pay the full purchase price plus stamp duty and costs to a total of $430,000.

In this example, I don’t need to combine the securities because I can fit it under the value of the home. However, the lender can require the investment property to be held as security for you to be allowed to use the rental income towards servicing. The bonus is that your LVR drops from 77% to 53% which can result in lower interest rates.

Home $1M + Investment $400k

Loan 1. $300,000 (Home)

Loan 2. $430,000 (Investment)

OR the standalone method

Home $1M

Loan 1. $300,000 (Home)

Loan 2. $110,000 (Investment)

Investment $400k

Loan 1. $320,000 (Investment)

Even if you choose to cross-collateralise to begin with, over time, as you reduce your principal and/or increase your values, you will be able to un-cross the securities until they are standalone – which then creates more equity for you to use. Using the above example, when the investment property value increases to $540,000 I can un-cross the securities so they’re both standalone.

It’s important that you understand the structure and its pros and cons so that you can make an educated decision around the potential risks for your long-term strategy.

Ultimately, cross-collateralising might be the strategy for you if;

- You’re just getting started on your investment portfolio

- You intend to keep your properties long-term

- You like the convenience of having your banking in one place

- You can use the strategy to leverage a better rate

But if you prefer to have more control over your property and financial position in the future, having an extra loan account and keeping the properties standalone could be your chosen strategy.

Talk to your friendly Broker about the strategy that suits your unique lifestyle and long-term plans.